Running a business is challenging, and paying less tax legally is always welcome news. From 1 January 2026, unincorporated businesses like sole traders and partnerships can benefit from a new 40% First-Year Allowance (FYA) on qualifying plant and machinery that aren’t fully covered by other allowances.

At Friendly Assist Accountancy, we help businesses make the most of these allowances so you can invest in your growth while reducing your tax bill.

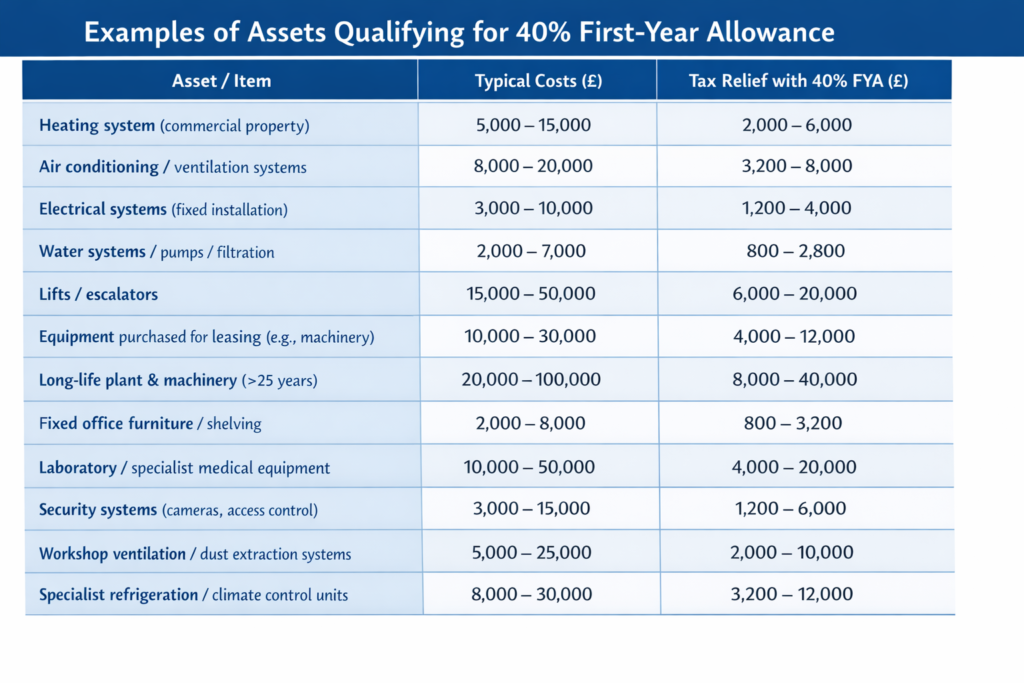

What Is the 40% First-Year Allowance?

The 40% FYA is a permanent tax relief that allows qualifying businesses to deduct 40% of the cost of new plant and machinery from taxable profits in the year of purchase.

Who benefits?

- Sole traders and partnerships who previously couldn’t access full expensing

- Businesses purchasing assets for leasing

- Assets included in the special-rate pool (fixtures, long-life equipment)

Example:

A self-employed landlord invests £20,000 in new heating and air conditioning systems for a rental property. These assets cannot be claimed under the AIA or full expensing, but with the 40% FYA, £8,000 can be deducted immediately from taxable profits. That’s a significant reduction in tax without waiting years for writing down allowances.

What Qualifies for the 40% FYA?

Assets that generally qualify include:

- Equipment purchased for leasing to others

- Building fixtures like heating, lighting, and air conditioning systems

- Long-life plant and machinery

- Certain assets not eligible for AIA or full expensing

This allowance complements the Annual Investment Allowance (AIA) and other capital reliefs, so you can combine them strategically to maximise savings.

Other Capital Allowance Options

While the 40% FYA is new and highly beneficial, businesses may also claim:

- Annual Investment Allowance (AIA): 100% relief on up to £1 million spent per year on qualifying plant and machinery

- Writing Down Allowances (WDA): Spread relief over time for assets not claimed under FYA or AIA

- Special Reliefs: Land Remediation Relief, Research & Development Allowances, Freeport/Investment Zone allowances

- Vehicle Allowances: 100% FYA for zero-emission cars and EV charging points until 2027

These options may still be useful depending on the mix and timing of your business asset purchases.

How We Can Help

At Friendly Assist Accountancy, we make claiming capital allowances simple:

- Identify which assets qualify for the 40% FYA and other reliefs

- Plan the timing of purchases to maximise your deductions

- Ensure accurate claims and compliance

- Review previous claims to check for missed opportunities

A short consultation could help you save thousands while ensuring your business stays compliant.

Useful Resources

For more information on qualifying assets and reliefs, see: